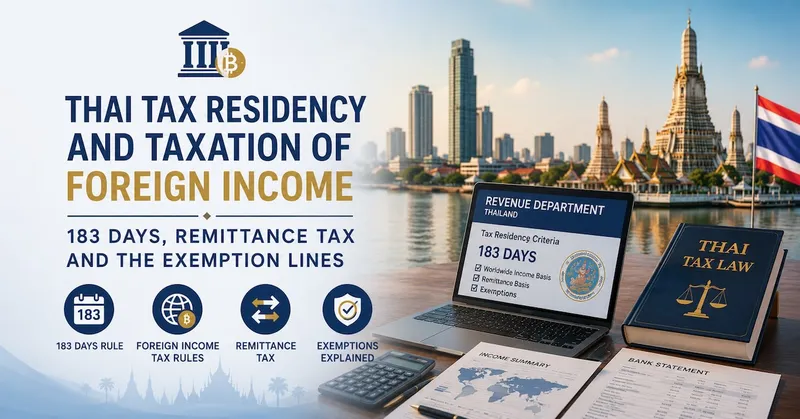

Thai Tax Residency and Taxation of Foreign Income: 183 Days, Remittance Tax and the Exemption Lines

Are You a Thai Tax Resident? The 183-Day Rule

The test is simple: spend 183 days or more in Thailand in a calendar year and you're a Thai tax resident for that year, regardless of your visa (tourist, Elite, retirement and work visas all count toward the days). A tax resident has filing obligations on Thai-source income and, under the new rules, on foreign income remitted into Thailand; a non-resident is generally taxed only on Thai-source income. Counting your days in Thailand is the first step in working out your tax obligation.

What the 2024 Rules Changed

- The common old practice was that "foreign income was tax-free if remitted into Thailand the following year," and many long-stayers arranged their money around it

- The Revenue Department's new interpretation (effective from the 2024 tax year) makes clear that a tax resident must include foreign income in personal income tax filing whenever they remit it into Thailand in a year they are a tax resident, no matter which year the income arose — the old "next-year exemption" no longer holds

- This isn't a new tax but a closing of the timing loophole; the precise implementation and interpretation remain per Revenue Department announcements and later guidance

What Counts as "Remittance," and Which Income Is Affected

- Remittance generally means bringing foreign funds into Thailand: wiring to a Thai account, carrying in and depositing, and certain uses of offshore funds in Thailand may be covered, with the boundary per the Revenue Department's interpretation

- Affected income types: foreign salary, business income, investment returns (dividends, interest, capital gains), overseas rental income and other personal-income-type foreign income

- Income not remitted into Thailand and left offshore is generally outside the current-period scope under the present framework — but once funds enter Thailand, filing comes into play, so plan ahead

Avoiding Double Taxation: Treaty and Tax Credits

- China and Thailand have a tax treaty (DTA): income already taxed abroad can usually claim a tax credit under the treaty to avoid full taxation on both sides — be sure to keep your tax-paid certificates

- Credits aren't automatic — you must declare correctly and provide proof when filing in Thailand, with applicability per the treaty terms and Revenue Department requirements

- Keep the route for exchanging and moving large funds into Thailand compliant and documented — see our Thailand currency exchange and remittance guide

Possible Exemptions and Planning Room

- Managing tax-residency status: under 183 days in a year means you're not a tax resident that year, but this needs a genuine residence arrangement, not a paper one

- Distinguishing principal from income: the new rules target "income," so remitting a portion of existing savings principal differs in nature from income — but the burden of proof is on you, requiring clear source-of-funds records

- The LTR long-stay visa: Thailand's BOI-led LTR (Long-Term Resident) visa carries specific tax benefits on foreign income for qualifying holders — worth assessing for high-income long-stayers

- All of the above are case-specific planning requiring calculation — consult a professional tax adviser before acting, and don't just copy old advice online

In Practice: How to File and Who to Use

- Annual personal income tax is filed on PND 90/91, and you need a Thai tax ID (TIN) before filing

- With remitted foreign income, organize the remitted amount, its nature and offshore tax-paid certificates, and have a professional accountant or tax adviser handle it

- Business owners must also separate the personal and company lines; for the company-side monthly and annual obligations see our monthly company tax and social-security guide and Thailand company accounting and tax filing guide

Frequently Asked Questions

I live here long term on a tourist/Elite visa — do I still pay Thai tax?

Tax obligation is about days, not the visa: 183 days or more in Thailand in a year makes you a tax resident, and Elite, retirement and tourist visas all count. Once a tax resident, foreign income remitted that year must be included in filing under the new rules. Which visa you hold doesn't change this test — many wrongly assume "no work visa, no tax," a common misconception. Whether you actually owe tax depends on income type, amount and treaty credits.

Does the "remit the following year, tax-free" trick still work?

No longer. From the 2024 tax year, the Revenue Department makes clear a tax resident must file foreign income remitted that year, regardless of when it arose — the old "wait until next year to remit" workaround is closed. The task now isn't to game the timing but to optimize lawfully via treaty credits, distinguishing principal from income, and compliant residence and visa planning, per the Revenue Department's current interpretation and professional advice.

If money I've already paid tax on in China is remitted to Thailand, do I pay again?

Not necessarily full double taxation. China and Thailand have a tax treaty, so income already taxed abroad can usually claim a credit when filing in Thailand to avoid double taxation — but the credit must be actively declared with tax-paid proof; it isn't automatic. Whether you owe additional tax, and how much, depends on the rate difference and income type — best left to a professional to calculate for your actual situation.

If I don't remit money into Thailand, is it entirely off my plate?

Under the current framework, foreign income not remitted into Thailand is generally outside the current-period scope, but that doesn't mean you can ignore it: first, funds must eventually be used, and filing arrives when they enter Thailand; second, the policy stance is evolving (whether it moves toward worldwide taxation remains to be seen). The safe approach is to plan your fund structure ahead, keep clear source records, and consult a professional regularly to track rule changes — rather than discovering the issue when you remit.

Need a Hand?

TaiHuBang provides tax consulting and filing support for individuals and businesses in Thailand: tax-residency assessment, filing for remitted foreign income, treaty-credit and compliant planning, and Thai tax ID registration and annual filing. We only do lawful, compliant tax planning and filing, all per the Revenue Department's current rules and professional advice. See our accounting and tax service, or submit an inquiry and a consultant will reply within 24 hours.

Related Articles

Monthly Compliance for Thai Companies: VAT Filing and Social Security

Registering a Thai company is only the start: every month brings fixed tax and social security obligations, and missed filings accumulate fines. This guide lays out the monthly, half-yearly and annual compliance calendar with cost references.

7/3/2026

Tax Refunds in Thailand: Tourist VAT Refund and Personal Income Tax Refund

Tourists can reclaim VAT on shopping when leaving Thailand, and expat workers may get overpaid income tax back through the annual filing. This guide covers eligibility, documents, procedures, and common rejection reasons for both.

7/3/2026

Money and Thailand: Currency Exchange, International Transfers and the FET Paper Trail

Exchange booths like Superrich beat airport and bank rates by a wide margin; property purchases must arrive as foreign currency with FET documentation or the transfer stalls at the Land Office. This guide compares exchange channels, covers sending money in and out of Thailand, and explains the tax rule on remitting foreign income.

7/3/2026